The Quarterly Pensions Investments Review is a comparison in expected risk and investment return.

Key Findings

- Comparing pension funds and regions: the expected returns of UK pension plans outperform those of their mainland European counterparts. This is driven by their high exposure to bonds and inflation-linked bonds, which are expected to perform well as long-term interest rates are anticipated to fluctuate around their recent (elevated) levels in most developed markets.

- Quarter-on-quarter outlook comparison: Global financial markets experienced initial gains followed by volatility due to the Middle East conflict, which raised inflation risks and growth concerns, leading to wider credit spreads, higher long-term interest rates, and surging commodity prices; near-term global growth is expected to be moderate with inflation rising due to energy prices, while equity and corporate credit returns are projected to be moderately positive but exposed to downside risks from geopolitical tensions and energy price disruptions.

- The update to the Ortec Finance Climate Scenarios highlights that rising physical climate risks can increase sovereign debt ratios and reduce bond returns and higher warming scenarios could lead to significant potential losses in private market investments.

- For details, please see below.

If you’re interested in learning how your pension fund is performing relative to others, please contact us for more information.

Expected Investment Performance – Risk and Return Results

The charts below show the expected investment return vs. the expected investment risk - from the top 30 largest pension funds per region.

Comparing pension funds and regions

Looking at general trends, the difference in expected returns between regions is stark. Expected returns and volatility among pension plans in North America and the UK are relatively high, while pension plans in Switzerland and the Netherlands show more moderate expectations.

This quarter, we focus our attention on the United Kingdom.

UK pension schemes have long been implementers of Liability-Driven Investment (LDI) strategies, including the use of swap products to reduce funding risks stemming from changes in liability values. At times, individual funds could be 100% hedged on both an inflation and interest rate basis. This has a significant impact on returns, as these swap products closely mimic the return on liabilities.

Given that the QPIR is an asset-only analysis, the impact of the LDI strategy is not reflected in the charts. However, it does offer a high-level indication of regional preferences when constructing portfolios.

The chart shows that the majority of UK pension plans have an expected return of around 6.50% — higher than most other regions. These funds tend to favor a substantial allocation to fixed income instruments, such as nominal and index-linked government bonds. On average, the top 30 UK pension funds have over 30% of their assets invested in such bonds, with two-thirds of that (approximately 20%) allocated to index-linked securities — double the allocation observed in the US and Canada.

This strategy is in line with regulatory directives: both private and public plans in the UK are required to discount their liabilities using yields from UK government securities. Minor adjustments can be made to reflect broader macroeconomic factors such as economic growth and wage inflation. By allocating to government bonds, UK pension funds naturally hedge against movements in liability values.

In contrast to the US, UK pension schemes have less flexibility in selecting a discount rate, which underscores a more standardized approach within the regulatory framework.

Additionally, indexation is guaranteed in the UK. This means that liability values rise in line with realized inflation, subject to caps or floors. This introduces a significant inflation risk — one that is not necessarily present in other regions such as the Netherlands. To mitigate this, UK pension funds allocate a considerable portion of their portfolios to index-linked bonds, creating a natural hedge against inflation. This strategic allocation reflects the proactive measures taken by UK pension funds to manage inflation-related uncertainty and enhance the long-term stability and resilience of their portfolios.

Energy shock shifts market focus from growth optimism to inflation and downside risks

Market developments and other events

Global equities posted gains early in the quarter, supported by resilient economic activity and moderating inflation, before reversing sharply as the conflict in the Middle East shifted market focus toward re-emerging inflation risks, a constrained monetary policy-path, and downside risks to growth. Markets exhibited heightened sensitivity to news-flow, with equity volatility rising alongside uncertainty.

Corporate credit spreads widened modestly across investment grade and high yield globally, retracing from historically tight levels, as inflation uncertainty increased, financial conditions tightened and growth expectations softened. The move was more pronounced in high yield, consistent with a broader repricing of risk premia.

Long term rates rose across major economies, driven by energy-led upward pressure in inflation expectations, higher real yields, and a repricing of the expected policy path. Term premia increased modestly amid fiscal concerns and expected debt issuance.

Commodity markets surged, led by energy prices as conflict disrupted regional infrastructure and supply routes. Gold initially gained as a safe haven before reversing as the US dollar strengthened and real yields rose.

Inflation declined across the US, euro area and UK early in the quarter, but the Middle East conflict reversed this trend through higher energy prices.

Outlook for growth, inflation, and interest rates

Global growth is expected to remain moderate and below trend. The energy-driven supply shock introduces downside risks in the near term, while geopolitical fragmentation weighs on productivity over the medium term. Tighter financial conditions and constrained monetary policy may further dampen growth, although fiscal stimulus, AI-driven investment and energy transition spending provide partial offsets.

Inflation is expected to rise in the near term due to higher energy prices and second-round effects through transport, food and input costs. Over the medium term, inflation is expected to moderate but remain above target due to persistent services inflation, fragmented supply chains and wage dynamics.

Long-term interest rates are expected to drift upward, driven by a repricing of the policy path and persistent inflation dynamics. Fiscal pressures and higher term premia add to upward pressure, particularly in the US where fiscal risks and labour market developments create uncertainty for monetary policy.

Outlook for financial assets

Equity returns are expected to be moderately positive in the near term, though upside is limited by geopolitical risks, higher commodity prices and negative sentiment.

Government bond returns improve modestly over the medium term due to higher yields, although returns remain constrained by inflation uncertainty and fiscal pressures.

Corporate credit returns are moderately positive, supported by higher spreads and improved carry, but remain sensitive to interest rate volatility and risk premia repricing.

Overall, the outlook remains exposed to downside risks, particularly if geopolitical tensions persist and energy prices continue to disrupt the disinflation path, increasing stagflationary risks.

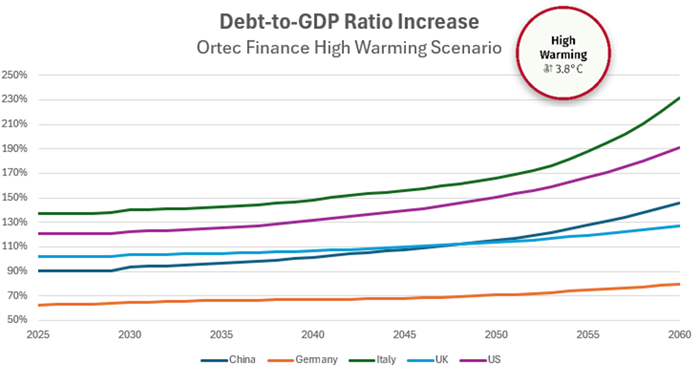

Pension funds warned on the impact of climate risk to sovereign debt and private assets in its 2026 climate scenario update

We released our annual update to our proprietary climate scenarios, now factoring in physical climate risk for sovereign debt.

Our High Warming scenario anticipates sharp and persistent GDP declines, shrinking tax revenues, and greater uninsured losses as result of rising physical risks. Figures show UK debt-to-GDP could rise from 102% in 2025 to 114% by 2050, and US ratios climbing from 121% to 151%. These pressures are expected to increase debt risk premia and interest rates, lowering bond returns and prompting downgrades in sovereign credit ratings.

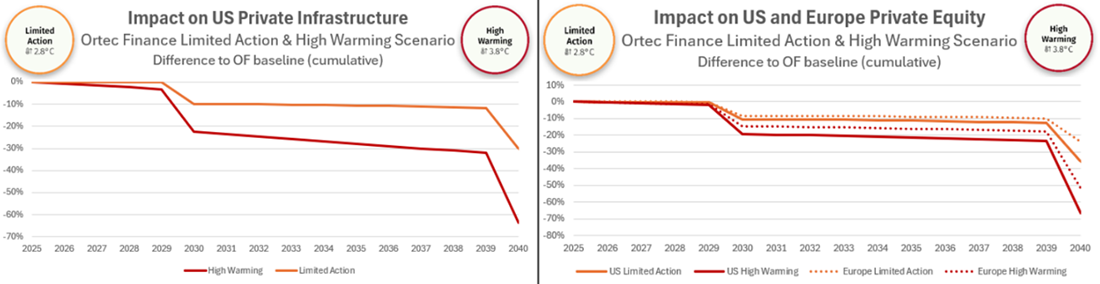

Pension funds need to understand climate impact to private assets under scenarios closest to the current trajectory of global warming

As pension funds seek better returns and governments urge local investment, fund managers are allocating more to private assets. Under a Limited Action scenario (2.8°C increase by 2100), US private infrastructure assets may see a 30% return loss over 15 years, in comparison to our baseline expectations*; this rises to over 60% in a High Warming scenario (3.8°C increase by 2100). In Europe, losses range from 15% (Limited Action) to over 30% (High Warming). US private equity underperforms by over 35% (Limited Action) and 65% (High Warming), while European private equity falls by over 20% and 50%, respectively.

Losses under these scenarios occur as longer-term physical risks begin to be priced into financial markets.

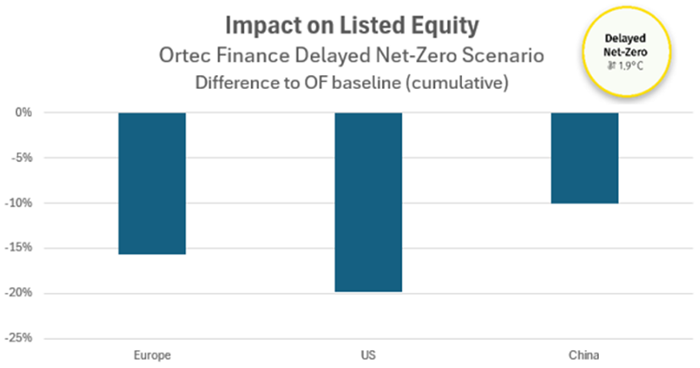

Delayed transition to net zero signals financial market disruption and sustained macroeconomic strain.

Ortec Finance’s analysis continues to indicate that achieving net zero by 2050 is no longer feasible, as highlighted in its 2025 update, pointing investors to focus towards its Delayed Net-Zero scenario.

Under Ortec Finance’s Delayed Net-Zero scenario, returns on European listed equities could decline by over 15% and US listed equities around 20% by 2030.

* The Ortec Finance Climate Scenarios are created as deviations from a baseline scenario (OF baseline) that reflects public reference climate scenarios in the 2°C to 3°C global warming range.

For more information or business inquiries, please reach out to Maurits van Joolingen.

Methodology and assumptions

This analysis is based on publicly available data, such as investment policy statements and annual reports, from the top 30 largest pension funds in Canada, the Netherlands, Switzerland, the UK, and the US.

The projections are made with GLASS Ortec Finance’s GLASS, a forward-looking Asset-Liability Management platform for institutional investors. Plan modeling is based on strategic asset allocations, mapped to public and private benchmarks, and rebalanced annually. For simplicity, active hedging strategies and derivatives are not included in the Quarterly Pension Review.

Returns shown are gross of management fees and expressed in the local currency of the relevant country.

The projections in this analysis are driven by the Ortec Finance Economic Scenario Generator.

Ortec Finance is a leading global provider of technology and solutions for risk and return management, enabling you to manage your investment decisions.

Discover our software and services for Pension Funds

Previous publications

Interested how pension funds have been performing over time? Then read our previous publications.

- Quarterly Pensions Investments Review - Q4 2025

- Quarterly Pensions Investments Review - Q3 2025

- Quarterly Pensions Investments Review - Q2 2025

- Quarterly Pensions Investments Review - Q1 2025

Contact

Elwin Molenbroek

Director, ALM Services

Drazen Pesjak

Senior Consultant Europe and Middle East