Lack of clarity around how climate change is priced in to financial markets is creating a significant roadblock for financial institutions attempting to mitigate climate-related risks in their asset allocations. According to a survey of almost 2,000 CFA professionals1, current valuations across all asset classes do not, at present, sufficiently reflect climate risk. Compounding the issue, many experts have indicated that mispricing is likely to persist for several years.

This poses a material risk for investors. The impact of sudden market adjustments could lead to overreaction and cascading sentiment shocks, potentially causing widespread market disruption and liquidity challenges across all asset classes.

Climate risks that have the potential to affect asset valuations are commonly classified into two primary categories: physical risk, caused by the changing climate and includes variations in temperatures and weather patterns; and transition risk, associated with the shift towards a low-carbon economy. While these facets are interlinked, it is important to understand how their impact upon current asset valuations differs.

Pricing in of climate transition risks (and opportunities) – The current state of play

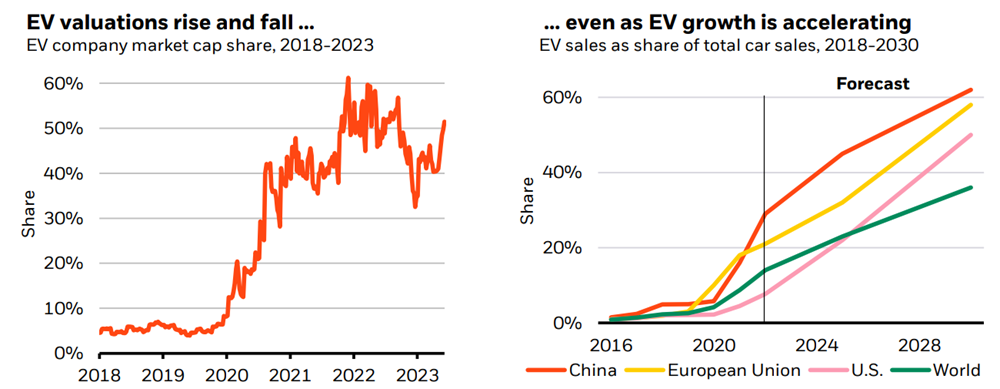

There have also been instances of the pricing in of initial overconfidence of an asset’s performance, such as the rapid valuation surge of electrical vehicle (EV) companies that took place from 2020, followed by a subsequent fluctuation and decline. EV company valuations have since stabilized to illustrate a more steady growth, which more accurately reflects their expected performance and overall market share.

Source: Blackrock Investment Institute, Tracking the low-carbon transition (July 2023), BII Investment perspectives (blackrock.com)

Pricing in of climate physical risks – The current state of play

Changes to asset valuations to reflect the financial and economic effects of long-term changes to weather, such as sea level rise and extreme weather events due to rising temperatures, are largely omitted by market participants, apart from some initial evidence showing a correlation between declining real estate valuations and the inability to secure insurance coverage.

This oversight arises from two challenges: individual investors struggle to assess their portfolio's physical risk exposure due to incomplete and insufficiently disclosed data, while fundamental disagreements between economists and climate scientists over the implications of various temperature pathways, further hinder any market efforts to price in its effects. Additionally, climate scientists warn that climate damages could accelerate in an exponential and disproportionate manner, particularly if critical climate tipping points are reached.

Without a general consensus on how to assess current and future physical risk impacts, there are signs that investors are inefficiently pricing in these risks due to the ambiguity surrounding an asset class’s level of physical risk exposure, rather than a lack of recognition of its crucial significance.

Are financial markets currently accurately pricing in climate risks?

It is challenging to determine which climate risks are currently being priced in and whether this is accurate or not due to uncertainty about future climate policies and their implementation, lack of statistical methods and available data, and incomplete information about climate consequences. This challenge is further compounded by a general tendency among financial market analysts operating within global financial markets to place limited focus on climate change until its impacts become material, typically at a local or regional level.

Research also indicates a key disparity in investor beliefs between brown assets and green assets. The valuation of brown assets currently appears to reflect a world that reaches a 2.5°C - 3°C temperature rise by 2100 in line with current policies, meaning the world will not meet its commitment under the Paris Agreement to limit temperature warming by 2100 to below 2°C. In contrast, green asset valuations reflect an outcome where this goal is achieved. Neither valuations are or will be necessarily correct, but this illustrates the fundamental difficulty for investors to understand whether each asset class has sufficiently priced in climate-related risks.

What could drive further pricing in of climate transition and physical risks?

A series of extreme weather events causing significant casualties and financial loss could drive more concrete transition policies. Academic studies have found that societies become much more willing to invest in decarbonization when they experience the effects of global warming on their economies and way of life firsthand. Major economies such as the US, EU, and China might rush to implement more ambitious transition policies or Nationally Determined Contributions (NDCs), leading to a mass selloff of brown assets in favor of green assets. Investors could also demand a stronger tilt towards green assets in response to market underperformance caused by extreme weather events, in anticipation of sudden low-carbon policy announcements, and/or to meet their self-imposed targets as members of net-zero investor alliance groups.

With climate risk currently causing only limited adjustments to asset valuations, such large-scale collective actions could lead to sudden, rather than gradual, pricing adjustments. This could have serious implications, for both financial markets and the real economy, particularly through the risk of stranded assets, market overreaction and pricing volatility. These implications have the potential to trigger a global financial crisis.

Conclusion: How can financial institutions respond to the currently limited and potential insufficient pricing in of climate risks within their investment portfolios?

Undertaking a climate scenario analysis that quantifies the impacts on asset classes and economies under various futures and incorporating different ways in which financial markets may respond to climate transition and physical risks, will provide crucial insights into a portfolio’s resilience. These insights can in turn, be used to develop robust and resilient strategies.

While asset valuations do not currently fully reflect climate risks, it is important to assess any impacts relative to the current pricing adjustments for climate transition risks that have already taken place. This approach helps objectively identify how impacts might differ under varying circumstances.

To address the underpricing of physical risks and align towards the pessimistic view of their implications, which reflects recent key academic publications, investors should consider using climate scenarios that adopt a logistic damage function like approach as proposed by Carbon Tracker and the Faculty and Institute of Actuaries. This approach captures stronger impacts compared to the quadratic approach, which tends to reflect the current, more optimistic views of economists on the severity of physical risk implications.

To address the underpricing of physical risks and align towards the pessimistic view of their implications, which reflects recent key academic publications, investors should consider using climate scenarios that adopt a logistic damage function like approach as proposed by Carbon Tracker and the Faculty and Institute of Actuaries. This approach captures stronger impacts compared to the quadratic approach, which tends to reflect the current, more optimistic views of economists on the severity of physical risk implications.

By comprehensively assessing potential financial market responses within the context of the current market environment, and adopting a pragmatic approach to evaluating physical risks, financial institutions will be better positioned to manage their portfolios effectively and address the systemic impacts arising from climate change.

Footnote:

[1] Bauer, R., K. Gödker, P. Smeets, F. Zimmermann, Mental Models in Financial Markets: How Do Experts Reason About the Pricing of Climate Risk? (May 28, 2024). European Corporate Governance Institute – Finance Working Paper No. 986/2024, https://ssrn.com/abstract=4851752More climate risk and sustainable finance insights

To receive the latest insights from our Climate Scenarios & Sustainability team on sustainable finance and climate risk management for financial institutions directly in your inbox, subscribe to our newsletter, Radar.

Contact

Bert Kramer

Head of Climate Research

Bronwyn Claire

Senior Climate SpecialistRelated Insights

-

05 June 2026Strategic Asset Allocation in the “TW-ICS” Era

05 June 2026Strategic Asset Allocation in the “TW-ICS” EraHow Taiwanese insurers can modernize strategic asset allocation and strengthen long-term resilience.

-

05 June 2026Total Portfolio Lens

05 June 2026Total Portfolio LensTotal Portfolio Lens (TPL) is built for investors navigating whole-fund complexity: it connects forward-looking analytics to action and allows investors to evolve at a pace that fits their governance and readiness.

-

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARL

01 June 2026Supporting PKZH in assessing the financial impact of an ESG exclusion policy using PEARLLearn how we supported PKZH, a Swiss pension fund in understanding the effect of an ESG exclusion policy on total fund performance.

-

01 June 2026Ortec Finance publishes its first Sustainability report

01 June 2026Ortec Finance publishes its first Sustainability reportOrtec Finance publishes its first Sustainability Report. It covers the reporting years 2024 and 2025.

-

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?

28 May 2026Captive Insurance vs Run-On: What Do the Numbers Say?In blog 6 in the series, we look at some specific case studies to highlight how alternative endgame arrangements can deliver meaningful financial benefits for both sponsors and members.

-

19 May 2026Total Portfolio Lens

This report introduces two closely related concepts that fill the gap between traditional SAA and full TPA.

-

13 May 2026Webinar recording: TPA Quick Wins

13 May 2026Webinar recording: TPA Quick WinsThis webinar explores TPA quick wins – practical steps that can be taken within existing frameworks to start capturing the benefits of TPA.

-

08 May 2026Quarterly Pensions Investments Review

08 May 2026Quarterly Pensions Investments ReviewThe Quarterly Pensions Investments Review is a comparison in expected risk and investment return.

-

07 May 2026Rethinking the Endgame for UK Defined Benefit Pension Schemes

Rethinking the Endgame for UK Defined Benefit (DB) Pension Schemes – Explore our blog series and discover how leading schemes are navigating the changing landscape.