Insurance companies issue guarantees that need to be valued according to option prices which capture market expectations. Moreover, for asset liability management and regulation purposes, insurers also need future values of these guarantees. The current common practice is to assume that the option implied volatilities remain constant when calculating future values. It is, however, well-known that these implied volatilities are not constant over time but depend on the state of the economy.

At Ortec Finance, we developed an approach that is able to determine future values of guarantees without assuming constant implied volatilities over time. Instead, the option market is driven by real-world indicators such as the VIX index and interest rates. By including these indicators, we are able to capture important stylized facts of the option market, for example, the implied volatility in the market increases during a financial crisis. These stylized facts will lead to more accurate estimations of future guarantee values.

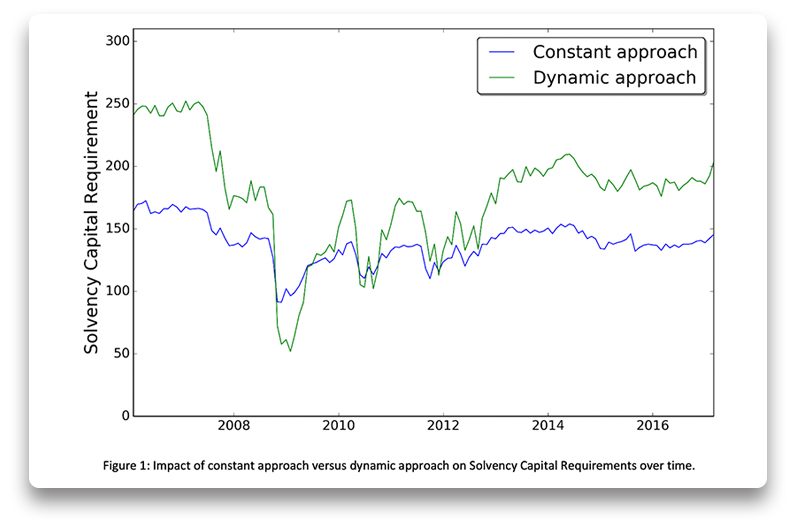

As an example, we demonstrate the impact of the approach on Solvency Capital Requirements. Compared to the constant implied volatility approach, the impact of the dynamic approach on the Solvency Capital Requirements varies between -46% to +52%, see Figure 1. More information on this topic can be found in our publication.

Related Insights

-

18 December 2024Climate change could erode Canadian pension fund returns by 44%

18 December 2024Climate change could erode Canadian pension fund returns by 44%Ortec Finance releases inaugural Canada pension fund climate risk report, analyzing the average portfolio allocation of the Top 30 pension funds in Canada by AUM

-

.png?w=576&hash=ACDB68A89AC45F798869837DDC9018AE) 17 December 2024Climate risk assessment – Top 30 Canadian pension funds

17 December 2024Climate risk assessment – Top 30 Canadian pension fundsDiscover how climate change impacts the top 30 Canadian pension funds through an analysis of their climate risk exposure, using Ortec Finance Climate Scenarios.

-

17 December 2024Assessing the climate risk exposure of pension funds and insurance companies worldwide

17 December 2024Assessing the climate risk exposure of pension funds and insurance companies worldwideAccess a series of Ortec Finance reports to examine how climate risk exposure and resilience vary among pension funds and insurance companies worldwide

-

17 December 2024PRESS RELEASE: US pension plans report possibility of increasing contributions despite improved funded status

17 December 2024PRESS RELEASE: US pension plans report possibility of increasing contributions despite improved funded status8% of pension plan managers say their funded status has improved over the past year, study shows

-

16 December 2024Climate risk assessment – Top 30 US pension funds

16 December 2024Climate risk assessment – Top 30 US pension fundsDiscover how climate change impacts the US pension fund industry through an analysis of their climate risk exposure, using Ortec Finance Climate Scenarios

-

16 December 2024US pension funds most sensitive to climate change

16 December 2024US pension funds most sensitive to climate changeOrtec Finance releases inaugural US pension fund climate risk report, analyzing the average portfolio allocation of the Top 30 pension funds in the US by AUM

-

11 December 2024Climate risk assessment – Top 30 UK pension funds

11 December 2024Climate risk assessment – Top 30 UK pension fundsDiscover how climate change impacts the top 30 UK pension funds through an analysis of their climate risk exposure, using Ortec Finance Climate Scenarios.

-

11 December 2024UK pension fund investment returns could reduce by 30% in a high warming stress scenario

11 December 2024UK pension fund investment returns could reduce by 30% in a high warming stress scenarioOrtec Finance releases inaugural UK pension fund climate risk report, analyzing the average portfolio allocation from the Top 30 pension funds by AUM

-

09 December 2024Climate risk assessment – European pension funds

09 December 2024Climate risk assessment – European pension fundsLearn how climate change impacts European pension funds, via an analysis on a reference portfolio that represents their average asset allocation.