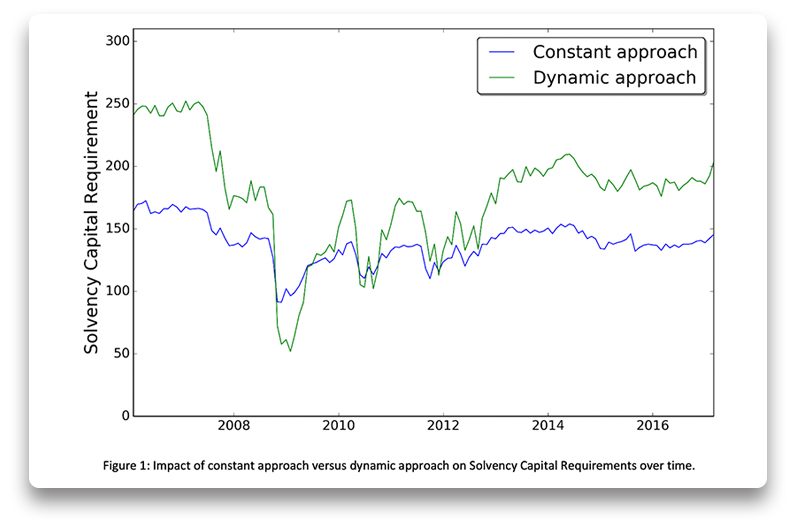

Insurance companies issue guarantees that need to be valued according to option prices which capture market expectations. Moreover, for asset liability management and regulation purposes, insurers also need future values of these guarantees. The current common practice is to assume that the option implied volatilities remain constant when calculating future values. It is, however, well-known that these implied volatilities are not constant over time but depend on the state of the economy.

At Ortec Finance, we developed an approach that is able to determine future values of guarantees without assuming constant implied volatilities over time. Instead, the option market is driven by real-world indicators such as the VIX index and interest rates. By including these indicators, we are able to capture important stylized facts of the option market, for example, the implied volatility in the market increases during a financial crisis. These stylized facts will lead to more accurate estimations of future guarantee values.

As an example, we demonstrate the impact of the approach on Solvency Capital Requirements. Compared to the constant implied volatility approach, the impact of the dynamic approach on the Solvency Capital Requirements varies between -46% to +52%, see Figure 1. More information on this topic can be found in our publication.

Related Insights

-

11 July 2025Webinar recording: Using traditional attribution methods to analyze ESG performance

11 July 2025Webinar recording: Using traditional attribution methods to analyze ESG performanceWatch our webinar to learn about a new ESG attribution model designed to help financial institutions integrate ESG impacts into their investment decision-making

-

09 July 2025Our perspective on the UK’s Pension Scheme Bill: Five key considerations for LGPS Funds

09 July 2025Our perspective on the UK’s Pension Scheme Bill: Five key considerations for LGPS FundsExplore Ortec Finance’s perspective on five key considerations particularly relevant to LGPS pools in the context of the UK’s largest pension reform.

-

09 July 2025Brightwell: Optimizing workflows and performance insights with PEARL

09 July 2025Brightwell: Optimizing workflows and performance insights with PEARLLearn how Ortec Finance helped Brightwell to establish investment performance and reporting as one of its core offerings under its new operational framework

-

08 July 2025PRESS RELEASE: AI role insurer’s investment strategy is growing rapidly, study shows

08 July 2025PRESS RELEASE: AI role insurer’s investment strategy is growing rapidly, study showsInsurers boost AI budgets to reshape investment strategy. Global study reveals key trend. See how AI is transforming asset allocation.

-

08 July 2025Quarterly Scenario webinar - 'How might investors manage ongoing policy uncertainty as the new normal?'

08 July 2025Quarterly Scenario webinar - 'How might investors manage ongoing policy uncertainty as the new normal?'Join us on July 24 for our Q2 webinar where our in-house expert Tom Janssen will be guiding you through our Quarterly Scenario outlook ‘How might investors manage ongoing policy uncertainty as the new normal?’ and Patrick Tuijp will discuss balance sheet stress testing in the global trade war era as our special topic.

-

07 July 2025The role of damage functions in assessing physical climate risks

07 July 2025The role of damage functions in assessing physical climate risksLearn how different damage functions affect the assessment of physical climate risks in climate risk modeling and investment decision-making.

-

07 July 2025In-House Student Day: Thursday September 19, 2024 - Rotterdam

07 July 2025In-House Student Day: Thursday September 19, 2024 - RotterdamCalling all students! Join us for an unforgettable day of insights and inspiration at our exclusive In-House Student Day.

-

26 June 2025PRESS RELEASE: Insurers intensify focus on stress testing, scenario modelling and asset liability management

26 June 2025PRESS RELEASE: Insurers intensify focus on stress testing, scenario modelling and asset liability managementPress release: Insurers ramp up investment in stress testing and scenario modelling. Global study highlights rising ALM budgets and outsourcing trends.

-

24 June 2025PRESS RELEASE: New report highlights evolving investment suitability practices in Canada

24 June 2025PRESS RELEASE: New report highlights evolving investment suitability practices in CanadaNew research report reveals how Canadian firms are evolving investment suitability post-CFRs—insights, gaps, and global comparisons.