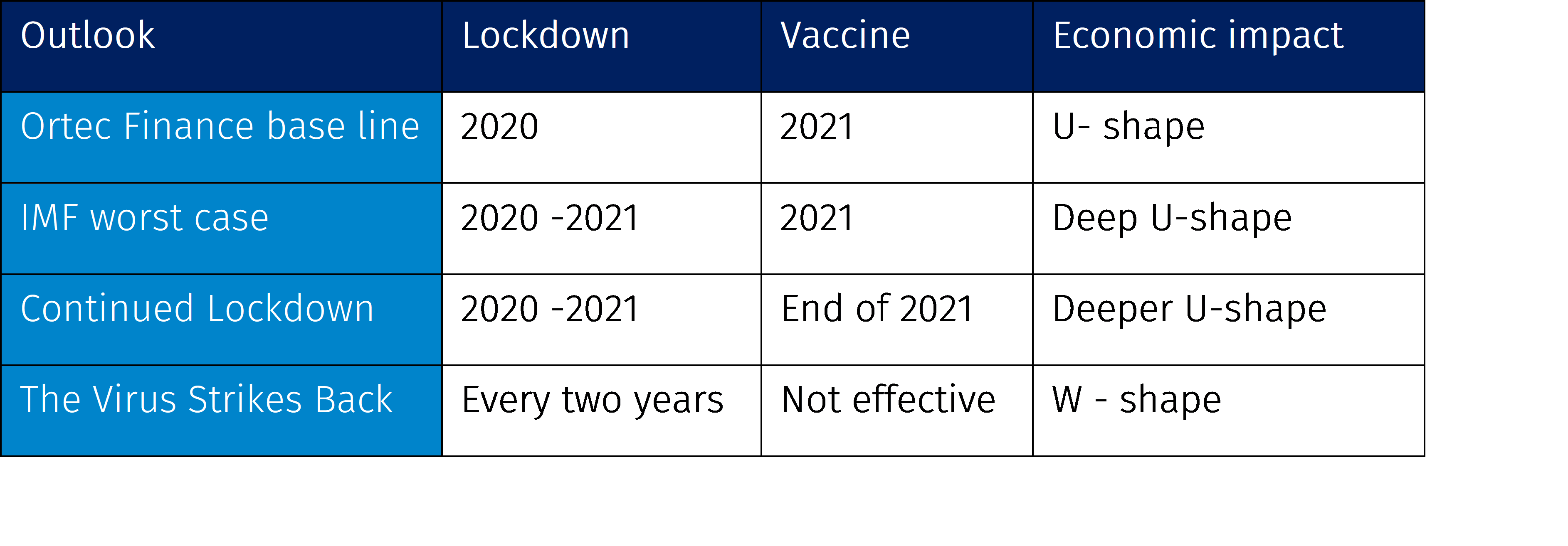

Informing management and the board on the possible financial consequences of this crisis by performing (what-if) scenario analysis is crucial in such a situation. For that purpose, Ortec Finance, in partnership with Cambridge Econometrics have defined four COVID-19 scenarios, including the year-by-year expected impact on economic and financial asset class returns per scenario.

How is your investment portfolio or solvency-ratio positioned for a deep economic recession yet with a steady recovery on the short and medium-term (1-5 years)? Pension and insurance companies can use these scenarios to assess the robustness of their investment portfolios and solvency position (e.g. for ORSA) for various COVID-19 scenarios. Get a head start and be fully informed, enabling you to enhance your decision-making process and improve discussions with your stakeholders.

More information?

Please download the whitepaper or contact:

Contact

Tessa Kuijl

Managing Director Goals-Based Wealth solutions

Patrick Tuijp

Head of Global Clients Scenarios & Asset Valuation

Edwin Massie

Senior ConsultantRelated Insights

-

17 April 2025Ortec Finance featured in CISL’s guide to building climate-resilient investment portfolios

17 April 2025Ortec Finance featured in CISL’s guide to building climate-resilient investment portfoliosOrtec Finance contributes to CISL’s guide developed in response to the growing need for investors to integrate physical climate risks

-

14 April 2025Ortec Finance updates climate scenarios

14 April 2025Ortec Finance updates climate scenariosOrtec Finance releases their 2025 climate scenarios which highlight important areas of developing physical and market pricing risks for institutional investors

-

10 April 2025Ortec Finance updates its performance measurement and attribution solution – PEARL 9.3

10 April 2025Ortec Finance updates its performance measurement and attribution solution – PEARL 9.3Ortec Finance upgrades its performance measurement and attribution solution to better integrate currency strategies into complex fund hierarchies

Contact

Contact

Tessa Kuijl

Managing Director Goals-Based Wealth solutions

Patrick Tuijp

Head of Global Clients Scenarios & Asset Valuation

Edwin Massie

Senior Consultant