Ortec Finance, a leading provider of top-down climate scenario analysis for financial institutions, today released its updated 2025 climate scenarios, which highlight several important areas of developing risk for institutional investors.

Net-zero by 2050 no longer realistic

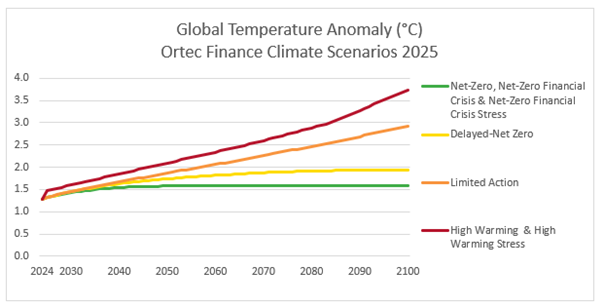

“Following the warmest year on record, the Paris Climate agreement target of limiting global temperature rises to 1.5°C by the turn of the century looks increasingly unlikely,” said Maurits van Joolingen, Managing Director, Climate Scenarios & Sustainability at Ortec Finance. “Even our most ambitious scenario does not anticipate the world reaching net zero until mid-2050 and shows temperatures rising by 1.6°C by 2100.”

Physical risk as a result of rising temperatures and emissions is the most serious threat to asset performance and the financial system. The medium to long-term impact of physical risk is far more pronounced in the scenarios that incorporate last year’s 0.2°C temperature spike and simulate the outcomes of the world’s current climate policies.

Inflation set to continue rising as GDP plummets

Increased physical risk will boost consumer price inflation. The High Warming scenario indicates that by 2050, price levels will be 11% higher in the US and 6% higher in the UK in comparison to Ortec Finance’s baseline (OF baseline) expectations*.

“Agricultural and labor productivity could suffer significantly as temperatures rise and long-term physical risk impacts increase. The combined effect could be highly inflationary to consumer prices,” said van Joolingen.

The High Warming scenario assumes the 2024 temperature spike will persist in the long term, further heightening chronic physical risk and negatively impacting GDP. He added, “Under this scenario, average global real GDP growth in the next 25 years is expected to drop to 1.1% - making it much harder for central banks to control inflation with monetary policy. This worsens in the following period up to 2070, where increasingly severe physical damage leads to almost zero real growth on average.”

Risk of rising credit defaults amid market disruption

The updated scenarios highlight how climate change could influence credit default rates during periods of market disruption, comparable to the GFC and dotcom crises. In the Delayed Net-Zero scenario, they show an initial uptick in investment-grade corporate bond defaults in 2030, sparked by a sudden step-up in policy action; however, under the High Warming scenario, where there is a lack of sufficient policy action to limit climate change, the impact from 2038 onward becomes far more severe, driven by the wider recognition of the scale of future climate risks.

Asset pricing to come under pressure in the medium term under current climate policies

The implications for asset repricing across countries and sectors are closely tied to their exposure to both transition and physical climate risks. Under the high warming scenarios, equity asset performance in the UK and US is anticipated to decline sharply in the 2030s due to an emerging insurance crisis, driven by the manifestation and increasing awareness of physical risks associated with rising temperatures. After a period of relative stability, equity prices are then expected to fall even more steeply in the late 2030s, driven by the impact of further escalating physical climate risks and insurers withdrawing from more markets.

Investment returns from low-carbon and renewable energy technologies are more resilient across all successful low-carbon transition scenarios

The results across all scenarios reflect shifts in the prevalence and adoption of low-carbon technologies, particularly renewable energy and electric vehicles. Since the previous iteration, the uptake of renewable energy has exceeded expectations, accompanied by a dramatic decline in costs. For instance, the cost of battery power dropped by 90% between 2010 and 2023**. The gap in projected equity returns because of different sector exposures to transition risk has never been more pronounced and creates opportunities for investors to realign portfolios to mitigate any fallout from the transition.

Maurits van Joolingen, Managing Director, Climate Scenarios & Sustainability at Ortec Finance, commented: “It is clear that under current policies, where there is hiatus in political willpower to reach net zero across large swathes of the developed world, temperatures will continue to break records. As a result, physical risk poses the greatest threat to institutional investment portfolios and the stability of the global financial system. The recent surge in global temperatures and corresponding risk of triggering a range of climate tipping points, accentuates the potential downside even further.

“Our latest release of scenarios are designed to help financial institutions fulfil their fiduciary duty to members and stakeholders by ensuring they fully understand climate change’s realistic impact across a broad range of potential outcomes and periods of market disruption. It also equips them with the tools to help mitigate the impact of climate change on their portfolios and identify opportunities for investing towards the low-carbon economy.”

* The Ortec Finance Climate Scenarios are created as deviations from a baseline scenario (OF baseline) that reflects public reference climate scenarios in the 2°C to 3°C global warming range.

** Source: Batteries and Secure Energy Transitions – Analysis - IEA

More about the 2025 Ortec Finance Climate Scenarios

Ortec Finance’s proprietary climate scenarios realistically assess a broad range of temperature pathways by 2100 and their associated systemic macroeconomic and financial market outcomes. These scenarios, developed in exclusive partnership with Cambridge Econometrics, simulate both a successful low-carbon transition and disorderly or failed transitions.

2025 Ortec Finance Climate Scenarios Climate Scenarios & Sustainability

Contact