Goal Priorities in Multi-Goal Based Planning

As financial advice shifts more and more to a client-centric approach, financial goals of clients are becoming increasingly important. Driven by regulations, bank and wealth managers must ensure the product they are selling matches the goals of their clients. In many cases, they use a ‘one pot – one goal’ strategy, determining one specific financial goal for each investment account. However, this is often not the reality. In many cases, especially in the private banking segment, an investor wants to achieve multiple goals with their current and future wealth. To provide the most fitting advice and fully adopt a goal-based approach, all the goals and priorities of the client should be taken into account. This can become a complex process, due to different timing of goals and the relative goal priorities.

For example, consider an investor, Mr Smith, who has one investment account that is designated for two different future goals. Mr Smith would like to buy a beach house in 2025 (priority ***), but he would also like to retire early, in 2030 (priority *****). Early retirement is his most important goal, while the beach house would be a nice extra. In other words, buying a beach house in 2025 should not jeopardize his early retirement. Because of the uncertain development of his capital, we do not know for sure if it is possible to buy the beach house in 2025 if he wants to retire in 2030.

Prioritizing goals

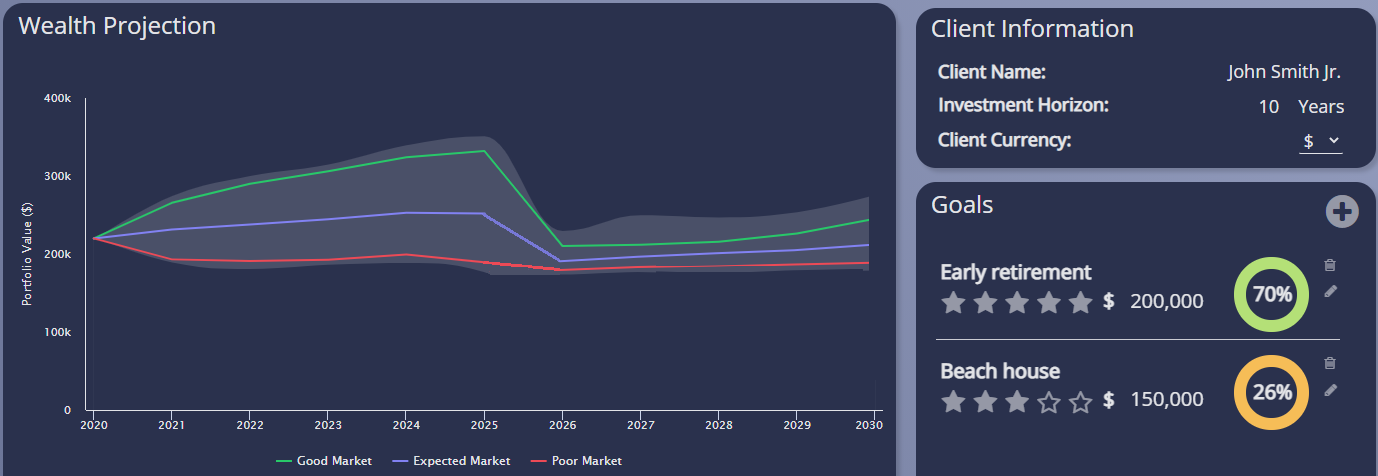

A commonly used method when advising for multiple goals is to use a static simulation for future growth of the capital and finance the goals as they happen over time. If there is enough capital to buy a beach house in 2025, the funds will be spent, no matter the effect on the goal later in time. A simulation of the capital under this assumption could look as follows:

Minimum reservation and expected budget

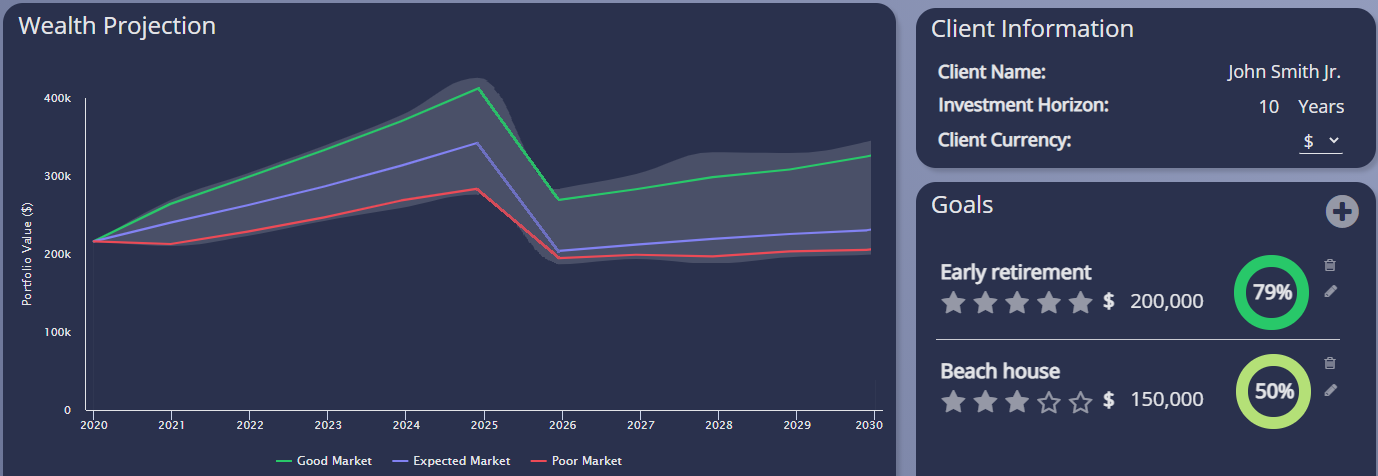

We will look at a strategy that is closer to what Mr Smith will most likely do in reality: he will only spend money on a beach house if this still gives him a high enough chance to realise his early retirement goal. To ensure that the retirement goal remains realistic, we should determine a minimum reservation. This reservation should be left in the account in 2025, after buying the beach house. For example, based on a number of simulations we can determine the minimum reservation in 2025, such that there is a probability of 70% that the early retirement goal is reached. Any capital above that minimum reservation can be spent on the beach house. This means that the budget for the beach house will vary, depending on the performance of the investments up until 2025. A simulation of the capital, when applying this strategy, could look as follows:

As an advisor, there are two major insights that you can provide your client based on this strategy. The first insight would be the minimum reservation of capital that should be left on the account to ensure the feasibility of a high priority goal. The second insight shows the expected budget that can be spent on a low(er) priority goal.

For example, in the case of Mr Smith, he originally wanted to buy a beach house worth € 150.000. As a result of the simulation, the advisor shows that he will need a minimum reservation in 2025 of € 200.000 to ensure his early retirement in 2030. Under expected market conditions, Mr Smith might be able to spend only € 90.000 on the beach house. However, when a poor economic scenario occurs and the investment portfolio generates a low or even negative return, Mr Smith might not be able to spend any money on a beach house. This is because in this scenario his account does not have €200.000 in 2025. If market conditions are favourable, Mr Smith might be able to spend the desired full amount of € 150.000.

Showing insights into the expected budget for the beach house in different economic market conditions is valuable information for the client, and provides a clear view of what to expect for both of his goals.

Monitoring insights and advice over time

In the strategy described above, an important aspect is that the investor has to take the minimum reservation for the highest priority goal into account, when spending money on the first goal. Because market conditions change, it is very important to monitor the results over time and to adjust the plan in case minimum reservations change. The closer the investor gets to his first goal, the better he can determine the exact minimum reservation that needs to remain in his account for the second goal.In the case of Mr Smith, he might not be satisfied with the low feasibility for his beach house goal. In order to improve the chances of reaching this goal, there are multiple steering variables he can use, like changing his risk profile, redefining his goal, or increase his monthly savings. For example, a monthly saving of € 1.000 increases the feasibility of his beach house to 50%. A simulation of the capital, when applying this strategy, could look as follows:

The additional savings have also improved the feasibility for the early retirement goal. Even without the additional savings, Mr Smith knows that he can most likely achieve his early retirement. This means that he can make a personal assessment if saving on a monthly basis is something he wants to do in order to buy the beach house.

Improve advice by taking goal priorities into account

By taking goal priorities into account when preparing financial advice for clients, advisors can suggest a minimum reservation on their client’s account. This can ensure there is a higher probability that high priority goals can be met later in time. In addition, advisors can provide insights on the expected budget that is available for low(er) priority goals. When monitoring these results over time, advisors can further improve the value and quality of advice towards their clients. By adopting an approach that fully puts client goals central in the advice process, the proposed strategy will also fully take the wishes and preferences of the client into account. A goal-based approach will provide a better conversation between advisor and client and can be communicated in a simple and more understandable way. This leads to a better and more suitable advice and as a result, increase client’s engagement and commitment to the plan.

For more information or details, do not hesitate to contact one of the authors:

Ronald Janssen: +31652065657 | Ronald.Janssen@ortec-finance.comEllen Schlebusch: +31107005460 | Ellen.Schlebusch@ortec-finance.com

Contact

Ronald Janssen

Managing Director Goals-Based PlanningRelated Insights

-

17 April 2025Ortec Finance featured in CISL’s guide to building climate-resilient investment portfolios

17 April 2025Ortec Finance featured in CISL’s guide to building climate-resilient investment portfoliosOrtec Finance contributes to CISL’s guide developed in response to the growing need for investors to integrate physical climate risks

-

14 April 2025Ortec Finance updates climate scenarios

14 April 2025Ortec Finance updates climate scenariosOrtec Finance releases their 2025 climate scenarios which highlight important areas of developing physical and market pricing risks for institutional investors

-

10 April 2025Ortec Finance updates its performance measurement and attribution solution – PEARL 9.3

10 April 2025Ortec Finance updates its performance measurement and attribution solution – PEARL 9.3Ortec Finance upgrades its performance measurement and attribution solution to better integrate currency strategies into complex fund hierarchies

-

10 April 2025Webinar: Utilizing PEARL 9.3 to further integrate currency strategies within complex fund hierarchies

10 April 2025Webinar: Utilizing PEARL 9.3 to further integrate currency strategies within complex fund hierarchiesLearn how Ortec Finance’s latest upgrade to its performance measurement and attribution solution can help asset owners further integrate currency strategies

-

04 April 2025Webinar recording: Fundamentals of currency decisions in performance attribution

04 April 2025Webinar recording: Fundamentals of currency decisions in performance attributionWatch our webinar to better understand how different decisions in currency overlay programs are impacting a portfolio’s overall performance

-

03 April 2025Investment suitability in Canada: Navigating the evolving regulatory environment

03 April 2025Investment suitability in Canada: Navigating the evolving regulatory environmentHow are top financial firms in Canada adapting to new suitability regulations? A new independent study reveals key insights.

-

03 April 2025Quarterly Scenario Webinar - 'Navigating the chaos in a shifting landscape'

03 April 2025Quarterly Scenario Webinar - 'Navigating the chaos in a shifting landscape'Join us on April 29 for our Q1 webinar where our in-house expert Finn Stijns will be guiding you through our Quarterly Scenario outlook ‘Navigating the chaos in a shifting landscape’ and Sophie Heald will be introducing the 2025 climate scenarios as our special topic.

-

03 April 2025Spring Statement 2025: Steering clients through the fiscal forecast before the storm hits

03 April 2025Spring Statement 2025: Steering clients through the fiscal forecast before the storm hitsSpring Statement 2025: Advisers must help clients navigate upcoming CGT, IHT, and pension reforms—preparing now ensures resilience in an evolving tax landscape.

-

03 April 2025PRESS RELEASE Ortec Finance boosts UK growth with appointment of Mark Glover

03 April 2025PRESS RELEASE Ortec Finance boosts UK growth with appointment of Mark GloverOrtec Finance deepens its commitment to the UK market with the appointment of Mark Glover as Managing Director – Head of UK Wealth Management.